At the beginning of July Fletcher School at Tufts University in collaboration with Mastercard, released the Digital Evolution Index (DEI17) which analyzes the state and rate of digital evolution across 60 countries. This evolution is the outcome of an interplay among four drivers – Supply Conditions, Demand Conditions, Institutional Environment, and Innovation and Change. The research captures about 170 indicators.

DEI17 reveals what are the patterns of digital evolution around the world and what factors explain these patterns, and how do they vary across regions; which countries are the most digitally competitive and which are the prime drivers of competitiveness: public or private sector?

By measuring each country’s current state of digital evolution and its pace of digital evolution over time (from 2008 till2015), the authors of the index created a map of our digital planet with four zones: Stand Out, Stall Out, Break Out, Watch Out. Some countries are at the border of multiple zones.

By measuring each country’s current state of digital evolution and its pace of digital evolution over time (from 2008 till2015), the authors of the index created a map of our digital planet with four zones: Stand Out, Stall Out, Break Out, Watch Out. Some countries are at the border of multiple zones.

Stand Out countries are highly digitally advanced and exhibit high momentum. They are leaders in driving innovation, building on their existing advantages in efficient and effective ways. However, sustaining consistently high momentum over time is challenging, as innovation-led expansions are often lumpy phenomena. To stay ahead, these countries need to keep their innovation engines in top gear and generate new demand, failing which they risk stalling out.

Stall Out countries enjoy a high state of digital advancement while exhibiting slowing momentum. The five top scoring countries in the DEI 2017 ranking — Norway, Sweden, Switzerland, Denmark, and Finland — are all in the Stall Out zone, reflecting the challenges of sustaining growth. Moving past these “digital plateaus” will require a conscious effort by these countries to reinvent themselves, to bet on a rising digital technology in which it has leadership, and to eliminate impediments to innovation. Stall Out countries may look to Stand Out countries for lessons in sustaining innovation-led growth. Countries in the Stall Out zone can put their maturity, scale, and network effects to use to reinvent themselves and grow.

Break Out countries are low-scoring in their current states of digitalization but are evolving rapidly. The high momentum of Break Out countries and their significant headroom for growth would make them highly attractive to investors. Often held back by relatively weak infrastructure and poor institutional quality, Break Out countries would do well to foster better institutions that can help nurture and sustain innovation. Break Out countries have the potential to become the Stand Out countries of the future, with China, Malaysia, Bolivia, Kenya, and Russia leading the pack.

Watch Out countries face significant challenges with their low state of digitalization and low momentum; in some cases, these countries are moving backward in their pace of digitalization. Some of these countries demonstrate remarkable creativity in the face of severe infrastructural gaps, institutional constraints, and low sophistication of consumer demand. The surest way for these countries to move the needle on momentum would be to improve internet access by closing the mobile internet gap — that is, the difference between the number of mobile phones and the number of mobile phones with internet access.

The Trust Landscape

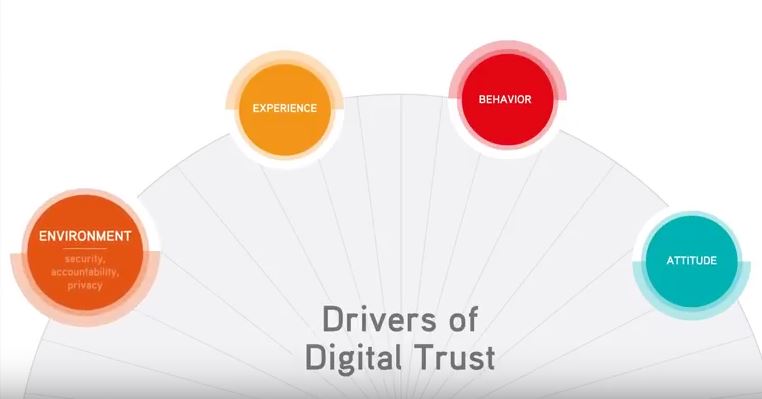

The DEI 17 index also captures capture the overall trust ecosystem supplied by governments and businesses—the guarantors of trust. Countries fall into four zones: High Trust Equilibrium, Low Trust Equilibrium, Trust Surplus, Trust Defecit.

The DEI 17 index also captures capture the overall trust ecosystem supplied by governments and businesses—the guarantors of trust. Countries fall into four zones: High Trust Equilibrium, Low Trust Equilibrium, Trust Surplus, Trust Defecit.

High Trust Equilibrium: Much like Stand Out nations, these countries are rare. Singapore, Spain, Norway, Hong Kong, and Finland all have users that exhibit patient and engaged behavior online combined with a more trustworthy environment and relatively seamless experience. They are in equilibrium because their level of trust—as exhibited through their behavior—matches the environment.

Low Trust Equilibrium: Among countries in the Low Trust Equilibrium zone such as Pakistan, Jordan, and Egypt, user trust—as exhibited through their behavior—matches the less trustworthy and more friction-laden environment. This could cause users in these countries tend to be less engaged and less patient with friction online.

Trust Surplus: Countries like China, Turkey, and Malaysia enjoy a Trust Surplus. They have patient and engaged users despite high friction experiences online and relatively less trustworthy environments. This Trust Surplus may be partially due to the high momentum many of these countries are experiencing—for many users, a slow smartphone is far superior to the lack of connectivity they may have lived with just a few years prior.

Trust Deficit: Countries in the Trust Deficit zone are similar to High Trust Equilibrium countries in terms of their experience and environments; however, users in these countries such as South Korea, US, France, and Australia tend to be less patient and fickle when faced with friction online.

Our Digital Planet Landscape

Digital technology is widespread and spreading fast. There are more mobile connections than people on the planet, and more people have access to a mobile phone than to a toilet. Cross-border flows of digitally transmitted data have grown manifold, accounting for more than one-third of the increase in global GDP in 2014, even as the free-flow of goods and services and cross-border capital have ebbed in the aftermath of the 2008 recession. While more people can benefit from access to information and communication, the potential for bad actors to create widespread havoc increases; with every year, the incidents of cyberattacks get bigger and have wider impact.

Digital players wield outsize market power. Based on their stock prices on July 6, 2017, Apple, Alphabet, Microsoft, Amazon, and Facebook were the five most valuable companies in the world. The most valuable non-American company, 7th overall, was China’s e-commerce giant, Alibaba Group. With products that rely on network effects, these players enjoy economies of scale and dominant market share. They have deep resources for innovation with the ability to accelerate the penetration and adoption of digital products.

Digital technologies are poised to change the future of work. Automation, big data, and artificial intelligence enabled by the application of digital technologies could affect 50% of the world economy. There is both anticipation and apprehension about what lies on the other side of the threshold of the “second machine age.” More than 1 billion jobs and $14.6 trillion in wages are automatable by today’s technology, which could open the door to new ways to harness human energy as well as to displacing routine jobs and increasing social inequities.

Digital markets are uneven. Politics, regulations, and levels of economic development play a major role in shaping the digital industry and its market attractiveness. With the world’s largest internet user population – 721 million – China has a parallel digital market because so many of the major global players have no presence there. India, with its 462 million internet users, has a digital economy representing arguably the greatest market potential for global players; however, it operates in multiple languages and multiple infrastructure challenges, despite the government having taken sweeping actions that affect the digital market. The European Union has 412 million internet users, but its market is fragmented; it is still in the process of creating a “digital single market.” In many countries, several websites or digital companies are blocked. Around the world, digital access itself is far from uniform: Barely 50% of the world’s population has access to the internet today.

Digital commerce must still contend with cash. Retail e-commerce sales worldwide are expected to hit $4 trillion by 2020, about double of where it is now. A major hurdle is the continuing stickiness of cash, which has not been displaced by digital alternatives despite myriad options. In 2013 85% of the world’s transactions were in cash. While the Netherlands, France, Sweden, and Switzerland are among the least cash-reliant countries in the world, even in the Eurozone, 75% of point-of-sale payments are in cash. Most of the developing world is overwhelmingly cash-dependent; in Malaysia, Peru, and Egypt, only 1% of transactions are cashless. Even India’s demonetization experiment has not broken the country’s heavy cash dependence. Five months after the country demonetized 86% of its currency, cash withdrawals were actually 0.6% higher than a year earlier.

Bulgaria on the Digital Map 2017

On the digital map, Bulgaria stands in the Break Out zone. The country experiences a relatively slow digitization, but is in a state of progress. Bulgaria has a strong impetus for growth and stands among the markets that are highly attractive to investors. Together with other countries in the Break Out list such as Italy, Poland, Brazil, Vietnam, Turkey, Latvia, Russia to name a few, Bulgaria was held back by a relatively weak infrastructure and insufficient institutional momentum for improvements. The countries in progress would have done well with a more active policy on the construction of a digitalized ecosystem and with policies that support the development of innovations. In this category, Bulgaria is among the countries with a strong potential to become part of the Stand Out countries of the Future.

With regard to the level of trust (an assessment of the overall ecosystem that combines digital behavior with the capabilities of the digital environment), Bulgaria ranks in the Trust Surplus zone together with China, Thailand, Turkey, Chile, New Zealand and more. Those countries enjoy motivated, patient and engaged users, although the digital ecosystem does not provide them them with smooth experiences online, and the digital environment is relatively less trustworthy.

Some of the key takeaways from DEI 17 evaluation:

- Use Public Policy as Key to the Success of the Digital Economy

Highly evolved countries typically have had strong government/policy involvement in shaping their digital economies. High momentum countries typically also have strong government/policy involvement. A sophisticated understanding of the state and drivers of the digital economy and its impact on the overall economy are essential for the success of a wide range of prominent policy imperatives such as: how Brexit negotiations are conducted; how India nudges its society towards a “less cash” future; and how the US and China compete for economic dominance.

- Identify and Amplify Drivers of Digital Momentum

Digital momentum is powered by different drivers depending on a country’s level of digital evolution and economic advancement. This has different implications for what advanced economies and developing economies ought to prioritize: innovation and institutions, respectively.

- Organize Digital Entrepôts As Linchpins of the Digital Planet

Smaller countries with strong institutions can create high value as early adopters and create a demonstration effect for the world by assembling the right ecosystem.

- Reinvent the Digital Stalwarts through Re-focusing on Innovation

The digitally most advanced countries can put their maturity, scale and network effects to use to reinvent themselves and grow.

- Play Digital Catch-Up by Closing the Mobile Internet Gap

The digitally least advanced countries must allocate limited resources wisely. Enabling internet access on the mobile phone provides the highest bang for the buck.

- Work Harder to Earn Users’ Trust in More Digitally Evolved Countries

Technology providers and policymakers offering privacy, security, and accountability may need to prioritize their marginal resources towards the more evolved countries with slowing momentum, where they risk losing users experiencing a “trust deficit.”

Download the full DEI 17 report at https://sites.tufts.edu/digitalplanet/files/2017/05/Digital_Planet_2017_FINAL.pdf